Yes, it’s still profitable. But it’s not as straightforward as it was five years back.

The HMO market in London has shifted. Costs to convert are up. Rules are stricter. Mortgage rates have come down a bit but are still much higher than in 2021. Article 4 Directions are also cropping up in more boroughs each year.

But the basics that make six-bed HMOs appealing remain. Room rents remain high. Young professionals are still looking for places to live. And HMOs still offer much better returns than standard buy-to-lets.

The real question isn’t if a 6-bed HMO can make money in London. It’s whether your project will stack up. That all comes down to the numbers.

What Does a 6-Bed HMO Actually Cost in London?

Let’s start with reality. A typical three or four-bedroom terraced house in outer London, the kind of property most investors convert, currently sells for around £425,000 to £525,000, depending on the borough and condition. Sutton, Croydon, Lewisham, Greenwich, and parts of Barking & Dagenham are popular hunting grounds.

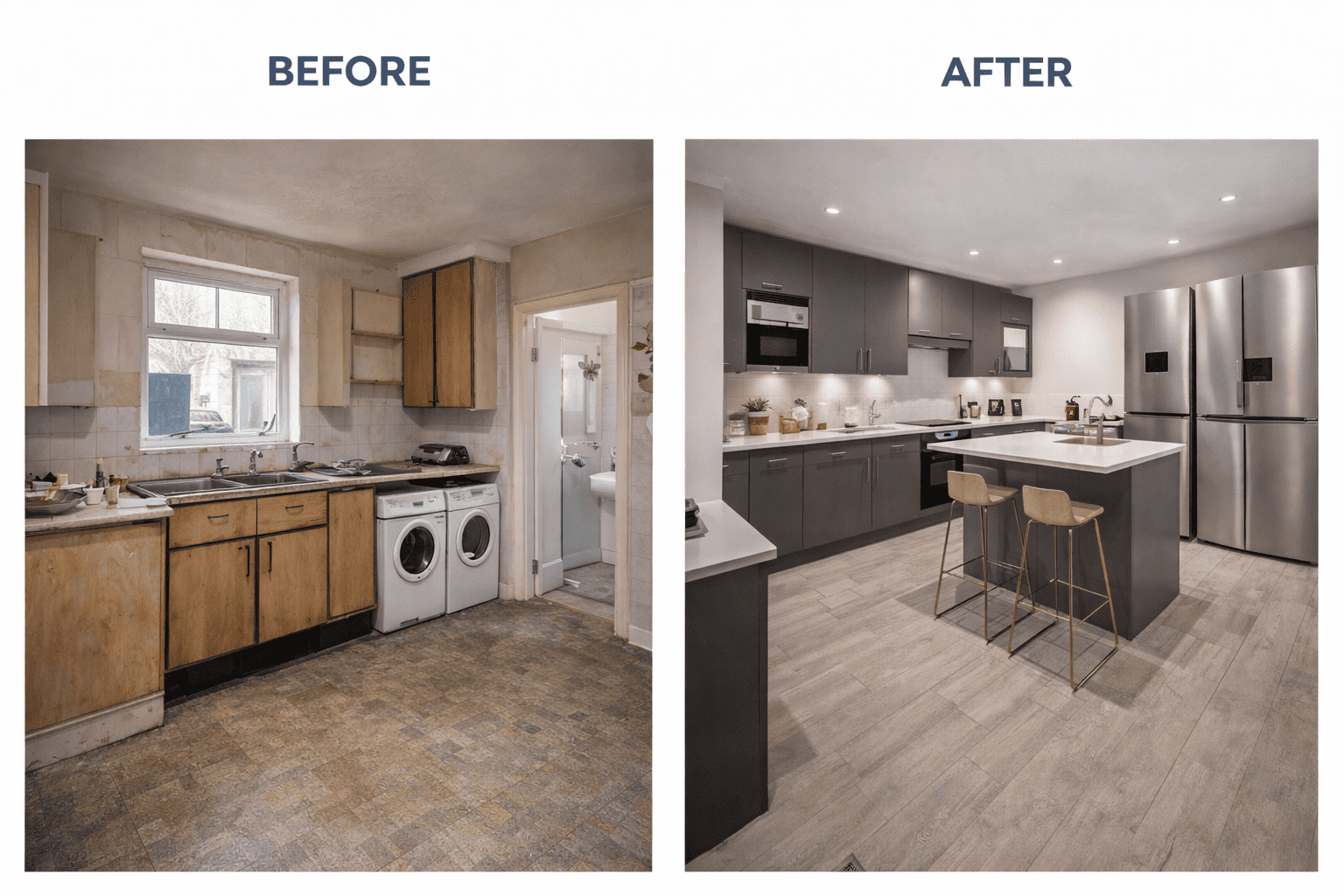

Turning that house into a six-bed HMO usually costs between £80,000 and £150,000 in London. This includes changing the layout, maybe adding a loft or rear extension, fitting kitchens and bathrooms, meeting fire safety rules, rewiring, and furnishing. Building costs in London are 20 to 40 percent higher than the UK average.

You’ll also need to allow for stamp duty, legal fees, surveys, professional fees like architects and planning, HMO licensing, and a 10 to 15 percent contingency. All together, you’re looking at a total investment of £550,000 to £700,000.

What Will It Earn?

This is where London’s HMO market stands out. Well-designed, well-managed HMOs in Zones 2 to 4 rent for £750 to £1,200 per room each month, depending on where they are, the finish, and if bills are included.

For a six-bed in outer London aimed at young professionals, you can safely estimate £850 per room. That’s £5,100 a month, or £61,200 a year before expenses. If you go for a higher spec in a better area, you could get £1,000 to £1,100 per room, which means £72,000 to £79,200 a year.

If you let the same house as a single-let, a three-bed in outer London might bring in £1,800 to £2,200 a month. That’s about £24,000 a year, which is less than half what you’d get from an HMO.

| Single Let (3-bed) | 6-Bed HMO | |

| Monthly income | £1,800 – £2,200 | £5,100 – £7,200 |

| Annual gross income | £21,600 – £26,400 | £61,200 – £86,400 |

| Estimated gross yield | 3.5% – 5% | 6.5% – 8%+ |

| Void risk | 100% income lost if empty | Spread across 6 tenancies |

How Does London Compare?

Let’s be straight: London doesn’t top the UK yield table. Research from Excellion Capital puts the average London HMO yield at around 6.6%, compared to 12.5% in the North East and 11.5% in the North West. Property prices in those regions are a fraction of London’s.

But yield isn’t the whole story. London usually sees better long-term price growth, stronger tenant demand, and higher rental income in pounds. A 6.6 percent yield on £600,000 can put more cash in your pocket than a 12 percent yield on £250,000, especially if rents keep rising.

And the Q4 2025 Pegasus Insight Landlord Trends data confirms that HMO landlords are still outperforming the wider market, generating average yields of 7.3% compared to 6.4% across all rental properties.

The Costs That Eat Your Margin

Gross yield is just the starting point. What you actually keep is another matter. Six-bed HMOs in London have running costs that often surprise new investors:

- Mortgage payments — specialist HMO rates in early 2026 sit in the mid-4% to low-5% range for fixed deals

- Bills (if included) — council tax, utilities, broadband, and cleaning of communal areas can run £800–£1,200 per month for a 6-bed

- Management fees — typically 10–15% of gross rent if you use a letting agent

- Maintenance and repairs — more tenants means more wear and tear

- Licensing fees — £500–£1,500 per five-year cycle, plus ongoing compliance costs

- Void periods — even a well-managed HMO will have some tenant turnover

After all costs, a well-managed London HMO usually gives a net yield of 4 to 6 percent. That’s about double what most standard buy-to-lets offer. But your profit depends on keeping costs down and rooms full.

What Separates Profitable Projects from Unprofitable Ones?

From working on HMO conversions across London, we notice the same patterns. The successful projects have a few things in common:

They buy in the right borough. Boroughs without Article 4 Directions (like Sutton, Camden, or Wandsworth) save you planning application costs and months of delays. Where Article 4 applies, successful investors account for it in their timeline and budget from the outset.

They design for the tenant, not just for compliance. A minimum-spec HMO that just scrapes past licensing requirements won’t command top rents. Properties with en-suites, good communal kitchens, and a professional finish consistently achieve £100–£200 per room per month more. Over six rooms, that’s an extra £7,200–£14,400 per year.

They get the conversion right the first time. Rework is expensive. Fire safety retrofits, failed planning applications, and layout redesigns mid-build all blow budgets. Working with an HMO-specialist builder who understands compliance from the start avoids these pitfalls.

They crunch the numbers before committing. The investors who run into trouble are the ones who buy first and budget later. You need to check the purchase price, conversion costs, realistic rents, and all running costs before you make an offer.

How hmoconversionbuilders Can Help

At hmoconversionbuilders, we help London investors turn properties into profitable, compliant six-bed HMOs. We handle everything: pre-purchase checks, layout design, planning support if needed, and the full build from strip-out to furnishing.

We always start with the numbers. We assess the property, estimate conversion costs, and help you work out the likely returns so you can decide before you spend any money.

If the numbers stack up, we design and build to a standard that attracts good tenants and strong rents. Fire safety, building rules, and licensing are part of the design from the start, not added on later.

Get in touch for a free, no-obligation chat. Whether you’re looking at your first HMO or growing your portfolio, we’ll help you see if a six-bed conversion makes sense for your property.

The Bottom Line

A six-bed HMO conversion in London is still profitable in 2026 — but only if you approach it as a business, not a gamble. The margins are tighter than they were a few years ago. Costs are higher, regulation is more stringent, and the bar for what tenants expect has risen.

But if you do your homework, pick the right property, and work with the right team, the returns are still some of the best in UK residential property. Demand is strong. Rental income is solid. A good conversion in the right spot will keep delivering for years.

Disclaimer: This article is for general informational purposes only and does not constitute financial or investment advice. Property values, rents, and costs vary by location and can change. Always carry out your own due diligence and consult qualified professionals before making investment decisions.